How the meal-kit delivery’s €6.75 billion industry convinced Europeans to subscribe to food quality

It’s around 5 PM on a Tuesday in Berlin, and Eric—VP of Marketing at a great media agency in Berlin—isn’t frantically Googling “quick dinner recipes” or spending on takeout. Instead, he and his partner are unboxing perfectly portioned ingredients for Thai green curry that promise a home-made-quality meal in a few minutes.

Their kids are setting the table. Nobody is stressed. Nobody spent 25 minutes at REWE after work. And somehow, dinner will be on the table before 6 PM.

This scene is multiplying across millions of European kitchens. The meal kit and prepared meal delivery market has become a €6.75 billion industry projected to triple to €20.78 billion by 2033—an 11.9% compound annual growth rate, according to market research firm Nova One Advisor.

In Germany alone, approximately 6.57 million people—13.1% of the population—now use meal kit services like HelloFresh, Juit, or PrepMyMeal.

Editor’s note: This analysis draws on research conducted by media agency GLADTOBE with consumer survey data from Global Web Index covering France, Germany, and the UK,, as well as independent market research from Mordor Intelligence, Grand View Research, Nova One Advisor, and Renub Research.

One Box, Three Europes

To understand how meal kits are taking over Europe, you have to realize they didn’t. The product may be the same, but the problem it solves is radically different depending on where it’s delivered. There is no such thing as a homogenous European consumer, and meal kits are a diagnostic tool revealing just how differently its major cultures approach the modern dilemma of dinner.

1. Germany: the optimization engine.

With nearly 20% of the European market, Germans embraced meal kits with characteristic efficiency. For them, it’s not a compromise; it’s a superior system. The country’s powerful environmental consciousness aligns perfectly with the promise of zero food waste from pre-portioned ingredients.

The user data confirms this pragmatic mindset. The German subscriber is part of an established, affluent household (€60-75k income), likely married (47%) with children (46%). They are planners who value reliability (52.3% want reliable brands) and trust (56.3% are loyal). Crucially, 60.3% are male, suggesting this isn’t about replacing tradition, but about couples jointly adopting a new, more logical household system. They’ve done the math, and at 41% buying at full price, they’ve decided the time savings justify the cost.

2. The UK: the inevitable upgrade.

The UK didn’t need to be convinced on convenience. With the highest meal kit penetration rate in Europe, services like Gousto and Mindful Chef are the next logical step in a culture that has long embraced practical food solutions. Ready meals already represent 41% of all red meat convenience products sold in the UK. The meal kit is simply a better version of what many were already doing—it offers more freshness, variety, and a touch of the gourmet without sacrificing the core benefit of speed. It’s the convenience economy reaching its premium, Instagrammable conclusion.

3. France & Italy: the traditionalist’s hack.

Here, the meal kit’s purpose is entirely different. It’s not about replacing the culture of food, but finding a modern way to access it. French consumers, initially skeptical of “industrial food,” were won over by services like Quitoque that focus on gourmet experiences and regional specialties. They aren’t selling convenience; they’re selling access to restaurant-quality techniques. In Italy, now Europe’s fastest-growing market (7.23% annually), kits emphasize authentic regional dishes—risottos and fresh pasta. It’s a shortcut not to an easier meal, but to a better one, for people who will pay for quality, just not for corners cut.

The New Kitchen Calculation

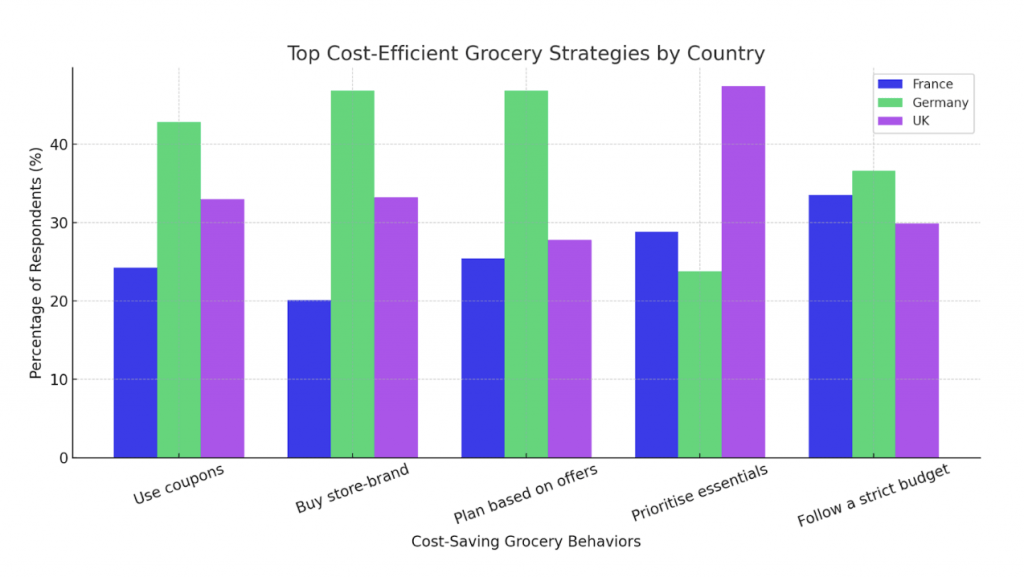

While cost-saving strategies like shopping at cheaper supermarkets are common (used by 44% of Germans and 43% of Brits), the meal kit subscriber exists in a different economic reality.

They are not impulse buyers. They are trading cost for two of the modern world’s most precious commodities: time and mental energy. The psychological shift is profound, as they treat meal subscriptions like they treat Netflix or Spotify—a recurring service that measurably improves their life. They aren’t comparing the per-meal cost to cooking from scratch; they’re comparing it to the alternative: mental exhaustion and an overpriced takeout order.

This has led to a market quietly dividing into consumer tribes:

- “Cook & Eat” kits (39.7% market share): For those who still want the experience of cooking.

- “Heat & Eat” meals (growing at 11.6%): The fastest-growing segment for ultimate convenience.

- Subscription Models (growing at 11.8%): The dominant delivery model, turning dinner into a utility.

The unseen forces driving growth

Beyond cultural nuances, several powerful, converging trends are fueling the entire category:

- The Vegan Elephant: Vegan meal kits are the fastest-growing category (12.9% annually). With 82% of nutrition experts identifying plant-based diets as the primary food trend, kits make it easy for consumers to try vegan cooking for health reasons (immunity, gut health) without a full dietary overhaul.

- The Pandemic Push: Lockdowns forced millions to try meal kits out of necessity. They discovered they liked them, and the behavior stuck.

- The Tech Backbone: This industry is impossible without a logistics revolution. AI-powered personalization, waste-reducing demand forecasting, and seamless mobile apps are the invisible architecture making it all work.

What’s Next

The market is past the novelty phase but not yet mature. The next chapter will see trends that deepen the cultural divisions, not erase them.

- Hyper-personalization: AI will customize meal plans based on fitness goals, health conditions, or even smartwatch data—a perfect fit for the German optimizer.

- The Medicalization of Food: As Europe’s population ages, expect functional meals for diabetic-friendly diets, menopause support, or cardiovascular wellness.

- Ghost Kitchens & Retail Convergence: The line between subscription and impulse will disappear. You can already find meal kits at Carrefour and Edeka, and soon you’ll order semi-prepared meals from a cloud kitchen for 10 minutes of finishing touches at home.

Meal kits aren't really disrupting how Europeans eat.

They're disrupting how Europeans think about cooking.

For generations, there was a clear hierarchy: restaurant food at the top, home-cooked in the middle, and convenience/prepared food at the bottom. Meal kits have created a new category that scrambles this ranking—they’re simultaneously home-cooked AND convenient, quality ingredients AND minimal effort.

In doing so, they’ve challenged a deeply European notion that good food requires suffering. That real cooking means spending Saturday at the market, Sunday preparing sauce, and weeknights stressed about what to make.

Maybe the real insight is that modern Europeans want the same thing everyone wants: to feel like they’re living well without having to be a chef, nutritionist, and meal planner on top of everything else.

The boxes showing up on doorsteps across Berlin, Paris, London, and Milan are delivering something more valuable than just ingredients: permission to care about food quality without letting it dominate your life.

And at €20 billion and counting, that permission is apparently worth paying for.

Data in this article comes from multiple industry reports including Mordor Intelligence, Grand View Research, Nova One Advisor, and Renub Research, as well as proprietary consumer survey data from GWI covering France, Germany, and the UK.